Microelectronic Insulators Market: Technological Advancements Driving Global Expansion 2025–2032

Microelectronic Insulators Market, Global Outlook and Forecast 2025-2032

MARKET INSIGHTS

The global Microelectronic Insulators Market was valued at US$ 1.87 billion in 2024 and is projected to reach US$ 2.94 billion by 2032, at a CAGR of 5.79% during the forecast period 2025-2032. The U.S. market accounted for 32% of global revenue in 2024, while China’s market is expected to grow at a higher CAGR of 9.2% through 2031.

Microelectronic insulators are specialized materials designed to prevent unwanted electrical conduction while providing thermal stability in semiconductor devices and electronic components. These materials play a critical role in integrated circuits, MEMS devices, and advanced packaging solutions by enabling electrical isolation, reducing crosstalk, and improving device performance. The primary insulator types include silicon dioxide (SiO2), silicon nitride (Si3N4), aluminum oxide (Al2O3), and emerging high-k dielectric materials.

The market growth is driven by increasing semiconductor demand across consumer electronics, automotive applications, and 5G infrastructure. The 0-100mm insulator segment currently dominates with over 45% market share due to widespread use in smartphone chipsets. Recent developments include Soitec SA’s 2024 launch of a new silicon-on-insulator (SOI) wafer technology, while Shin-Etsu Chemical has expanded its high-purity quartz production capacity to meet growing semiconductor fabrication demands.

List of Key Microelectronic Insulator Companies Profiled

- Soitec SA (France)

- Coorstek Inc. (U.S.)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- SunEdison Inc. (U.S.)

- Murata Manufacturing Co., Ltd. (Japan)

- Kyocera Corporation (Japan)

- Ametek Inc. (U.S.)

- NGK Insulators, Ltd. (Japan)

- Tong Hsing Electronic Industries (Taiwan)

Segment Analysis:

By Type

0-100mm Segment Leads Due to High Demand in Miniaturized Electronic Devices

The market is segmented based on type into:

- 0-100mm

- Subtypes: Thin-film insulators, ceramic substrates, and others

- 100-300mm

- Above 300mm

By Application

Consumer Electronics Segment Dominates with Increasing Adoption in Smart Devices

The market is segmented based on application into:

- Automobile and Smart Industry

- Consumer Electronic

- Others

By Material

Ceramic Insulators Hold Major Share Due to Superior Thermal and Electrical Properties

The market is segmented based on material into:

- Ceramic

- Subtypes: Alumina, zirconia, and others

- Glass

- Polymer

- Others

By End User

Semiconductor Manufacturers Dominate as Primary Consumers of Microelectronic Insulators

The market is segmented based on end user into:

- Semiconductor manufacturers

- Electronic component suppliers

- Research institutions

Regional Analysis: Microelectronic Insulators Market

North America

North America dominates the microelectronic insulators market with a strong presence of semiconductor manufacturers and technology leaders in the U.S. The region benefits from extensive R&D investments, accounting for approximately 40% of the global semiconductor research expenditure. Stringent quality standards and the presence of companies like SunEdison drive demand for high-precision insulating materials. The CHIPS Act, allocating $52 billion for domestic semiconductor production, will further boost microelectronic insulator consumption. However, supply chain dependencies on Asian raw material suppliers create pricing volatility challenges. The emphasis on next-gen 5G and IoT applications propels innovation in thermally efficient insulating substrates.

Europe

Europe maintains steady growth in the microelectronic insulators sector through its automotive electronics and industrial automation sectors. Germany’s leadership in automotive MEMS sensors utilizes advanced ceramic insulators, while the EU’s Horizon Europe program funds €1.9 billion for semiconductor material research. Strict REACH regulations push manufacturers toward lead-free and halogen-free insulating compounds. The region faces pressure from Asian competitors on pricing, prompting local players like Soitec SA to focus on specialty SOI (silicon-on-insulator) wafers for premium applications. Energy efficiency directives for consumer electronics additionally stimulate demand for low dielectric constant materials.

Asia-Pacific

As the largest consumer of microelectronic insulators, Asia-Pacific accounts for over 60% of global demand, driven by semiconductor foundries in Taiwan and China’s OSAT (outsourced semiconductor assembly and test) facilities. Japan’s Shin-Etsu Chemical leads in high-purity quartz crucibles for silicon wafer production, while Southeast Asia emerges as a packaging material hub. India’s semiconductor mission, targeting $300 billion in electronics production by 2026, will create new insulator demand, though local material science capabilities remain underdeveloped. Cost competition intensifies as Chinese domestic suppliers expand 200mm and 300mm insulating substrate capacities, potentially disrupting traditional supply chains.

South America

The South American market shows niche potential in automotive and medical electronics applications, with Brazil’s semiconductor packaging sector growing at 8% annually. Limited local wafer production means most insulators are imported, primarily from U.S. and Asian suppliers. Argentina’s burgeoning IoT device assembly creates opportunities for thermal interface materials, though currency fluctuations and import barriers hinder consistent market growth. Regional free trade agreements may improve material accessibility, but infrastructure gaps in testing and certification facilities delay advanced insulator adoption compared to other regions.

Middle East & Africa

This emerging market focuses primarily on downstream electronics assembly rather than front-end semiconductor manufacturing, creating demand for basic insulating substrates in consumer electronics. Israel’s thriving semiconductor design industry drives specialty material needs, while UAE’s investment in smart city infrastructure requires durable insulators for harsh environments. South Africa serves as a gateway for imported materials into the continent, though low local production capabilities keep prices elevated. The region’s growth potential ties closely to foreign direct investment in electronics manufacturing, currently concentrated in North African nations with EU trade agreements.

MARKET DYNAMICS

The transition to advanced packaging technologies like 3D IC and chiplet architectures presents significant technical challenges for insulator manufacturers. Thermal expansion mismatches between insulating materials and semiconductor substrates can cause reliability issues, particularly in high-temperature applications. Approximately 15-20% of advanced packaging failures can be attributed to insulating material performance limitations, driving the need for continued material innovation.

Shortage of Specialized Talent

The industry faces a critical shortage of materials scientists and process engineers with expertise in advanced insulator technologies. This talent gap is particularly acute in emerging markets where educational infrastructure has not kept pace with industry requirements.

Testing and Validation Bottlenecks

Comprehensive reliability testing of new insulating materials typically requires 12-18 months, creating significant delays in time-to-market. The lack of standardized testing protocols across different applications further complicates the qualification process.

The growing renewable energy sector presents significant opportunities for microelectronic insulator manufacturers. Large-scale battery storage systems and solar inverters require specialized insulating materials capable of withstanding high voltages and extreme environmental conditions. The global energy storage market is projected to grow tenfold by 2030, creating substantial demand for advanced insulating solutions in power conversion applications.

Emerging computing paradigms like quantum computing and neuromorphic chips require entirely new approaches to electronic insulation. These applications demand materials with unprecedented purity levels and dielectric properties, opening opportunities for manufacturers capable of pushing material science boundaries. Several leading research institutions have established partnerships with material suppliers to co-develop specialized insulating solutions for these futuristic computing platforms.

With semiconductor manufacturing capacity expanding rapidly in Southeast Asia and the Middle East, microelectronic insulator manufacturers have significant opportunities to establish localized production facilities. Government incentives and growing domestic demand make regions like India and Vietnam particularly attractive for new investments, potentially reshaping the global supply chain landscape in coming years.

The market is highly fragmented, with a mix of global and regional players competing for market share. To Learn More About the Global Trends Impacting the Future of Top 10 Companies https://semiconductorinsight.com/download-sample-report/?product_id=88030

FREQUENTLY ASKED QUESTIONS:

- What is the current market size of Global Microelectronic Insulators Market?

- Which key companies operate in Global Microelectronic Insulators Market?

- What are the key growth drivers?

- Which region dominates the market?

- What are the emerging trends?

Related Reports:

https://semiconductorblogs21.blogspot.com/2025/07/gas-scrubbers-for-semiconductor-market_17.html

https://semiconductorblogs21.blogspot.com/2025/07/mosfet-output-optocoupler-market.html

https://semiconductorblogs21.blogspot.com/2025/07/high-linearity-optocoupler-market.html

https://semiconductorblogs21.blogspot.com/2025/07/single-color-mid-power-leds-market.html

https://semiconductorblogs21.blogspot.com/2025/07/multi-mode-fiber-optic-connector-market.html

https://semiconductorblogs21.blogspot.com/2025/07/led-interactive-touch-screen-market.html

https://semiconductorblogs21.blogspot.com/2025/07/biometric-security-ssd-market-regional.html

https://semiconductorblogs21.blogspot.com/2025/07/vr-graphics-card-market-regulatory.html

https://semiconductorblogs21.blogspot.com/2025/07/1080p-graphics-card-market-increasing.html

https://semiconductorinsight.com/download-sample-report/?product_id=42086https://semiconductorblogs21.blogspot.com/2025/07/high-power-infrared-emitter-market.html

https://semiconductorblogs21.blogspot.com/2025/07/high-speed-card-edge-connector-market.html

https://semiconductorblogs21.blogspot.com/2025/07/digital-speed-sensor-market-strategic.html

https://semiconductorblogs21.blogspot.com/2025/07/miniature-compression-load-cell-market.html

https://semiconductorblogs21.blogspot.com/2025/07/analog-measurement-module-market-rising.html

https://semiconductorblogs21.blogspot.com/2025/07/power-measurement-module-market-growth.html

CONTACT US:

City vista, 203A, Fountain Road, Ashoka Nagar, Kharadi, Pune, Maharashtra 411014

[+91 8087992013]

[email protected]

Catégories

Lire la suite

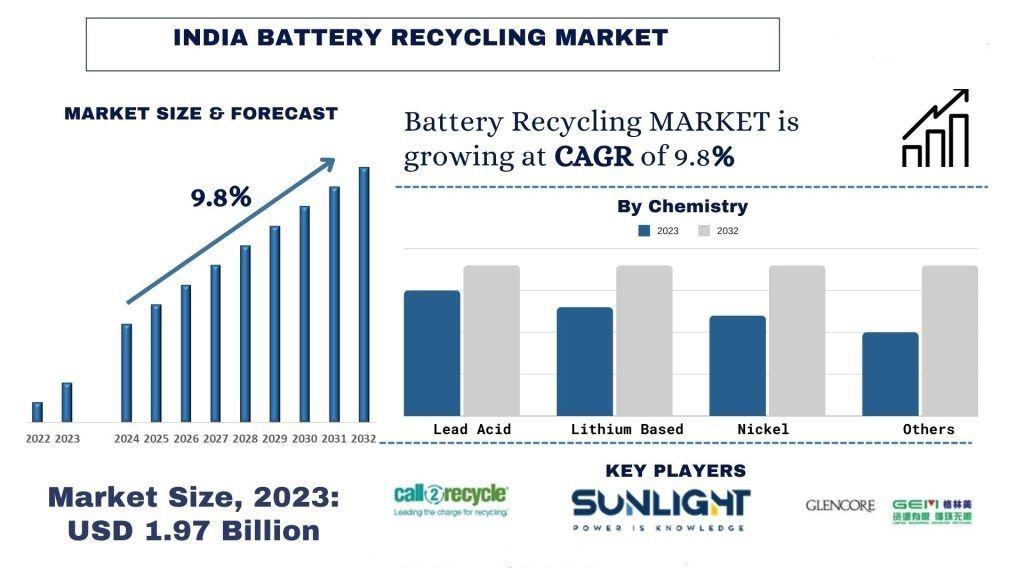

According to the UnivDatos, the increasing number of electric vehicles in India will drive the growth scenario of battery recycling and as per their India battery recycling market report, the market was valued at USD 1.97 billion in 2023, growing at a CAGR of 9.8% during the forecast period from 2024 - 2032 to reach USD billion by 2032. Access sample report (including graphs, charts, and...

Artificial Intelligence in Fintech Market, By Component (Solutions and Services), Deployment Mode (Cloud and On-Premises), Application (Virtual Assistant, Business Analytics and Reporting, Customer Behavioural Analytics and Others) – Industry Trends and Forecast to 2029. Data Bridge Market Research analyses that the artificial intelligence in fintech market value, which was USD 13.14...

In today's rapidly evolving digital landscape, on-demand clone apps have emerged as a powerful solution for entrepreneurs looking to capitalize on successful business models with minimal development time and cost. By leveraging existing frameworks and technologies, these apps allow businesses to quickly enter competitive markets and meet consumer demands effectively. The role of technology in...

If you’re seeking best makeup artist courses in London, UK that offer personalized instruction and industry-relevant experience, CBMA academy is the ideal choice. The CBMA academy’s makeup classes in London are designed to give you practical, on-set experience, ensuring you’re well-prepared for a successful career in makeup artistry. Professional Makeup Courses in London...

North America Immunoassay Reagents and Devices Market Segmentation, By Technology (Enzyme immunoassays, Fluorescent immunoassays, Chemiluminescence immunoassays and Radioimmunoassay), Product (Analyzers and Reagents), Application (Oncology, Infectious diseases, Cardiology, Bone and mineral, Endocrinology, Autoimmunity, Toxicology, Hematology and Neonatal screening), End users (Hospitals,...