Top Tips for Renting Small Business Space: Find the Right Fit for Your Startup

Launching a startup is an exciting milestone, but one of the most critical decisions you’ll face is choosing the right business space. The location and type of commercial space you rent can either set the stage for long-term success or become a costly misstep. Whether you're opening a retail shop, office, or production facility, finding the perfect rental space that matches your budget and business model is essential.

In this comprehensive guide, we’ll share the top tips for renting small business space for rent, with a focus on helping startups navigate the process effectively. By the end, you’ll have the knowledge to confidently evaluate spaces, negotiate leases, and secure a location that fuels your growth.

1. Understand Your Business Requirements

Before browsing commercial listings or talking to landlords, you must clearly define your startup’s physical needs. Ask yourself:

-

What is the primary function of the space? Retail, office, production, or hybrid?

-

How many employees or customers will be using the space?

-

Do you require specialized features such as high ceilings, loading docks, or kitchenettes?

-

How much square footage is necessary to operate efficiently?

Knowing your space requirements prevents you from overpaying for extra features you don’t need or being stuck in a location that restricts your operations.

2. Determine Your Budget

Renting commercial space comes with ongoing costs that can significantly impact your startup's cash flow. It's crucial to define a clear budget before you begin your search.

When calculating your budget, consider:

-

Base monthly rent

-

Security deposit

-

Utility bills

-

Insurance premiums

-

Maintenance and repairs

-

Property taxes and association fees (if applicable)

A common rule is that rent should not exceed 5-10% of your projected monthly revenue. Build in a buffer for hidden expenses, especially during the first few months when revenue might be inconsistent.

3. Choose the Right Location

Your startup’s success may depend heavily on your location. The perfect spot is one that offers visibility, accessibility, and aligns with your brand identity. Consider the following:

-

Foot traffic: For retail or customer-facing startups, visibility and foot traffic are essential.

-

Proximity to your target market: Is the area frequented by your ideal customers?

-

Competitors: Is it beneficial to be close to competitors, or should you avoid them?

-

Accessibility: Is it easy for customers and employees to find parking or access public transportation?

Take time to visit prospective areas during different times of the day and week to observe activity levels, noise, safety, and overall energy.

4. Work With a Commercial Real Estate Agent

While you can search online for available commercial properties, a seasoned commercial real estate agent can be invaluable. They’ll help you:

-

Navigate the market

-

Access off-market listings

-

Understand zoning and permits

-

Negotiate favorable lease terms

Choose an agent who understands the needs of startups and is familiar with your target neighborhood.

5. Explore Flexible Lease Options

Startups often deal with uncertainty. Your space requirements may change quickly as your business grows. That’s why flexible leasing options are worth exploring.

Some of the best options for startups include:

-

Short-term leases: Provides the flexibility to upgrade or move as needed.

-

Shared office spaces: Ideal for freelancers, consultants, or tech startups that don’t need a large footprint.

-

Subleases: These are often more affordable and come with shorter commitments.

Flexibility can prevent you from getting locked into a lease that no longer fits your evolving needs.

6. Inspect the Space Thoroughly

Before signing a lease, visit the space in person and conduct a detailed walkthrough. Look for:

-

Structural issues (cracks, leaks, mold)

-

Electrical wiring and outlets

-

Heating, ventilation, and air conditioning (HVAC)

-

Internet connectivity options

-

Security features (locks, alarms, lighting)

-

ADA compliance and accessibility

Bring in a contractor or inspector if needed. Fixing infrastructure problems can be expensive and delay your launch if not discovered in advance.

7. Understand Zoning and Legal Requirements

Zoning regulations dictate what types of businesses can operate in specific areas. Before you commit, check that your intended use aligns with the property's zoning.

Steps to take:

-

Contact local city planning or zoning departments

-

Confirm allowable uses of the space

-

Check if any special permits or licenses are required

-

Understand local health, safety, and occupancy codes

Failure to comply with zoning regulations can result in fines or even forced closure.

8. Compare Multiple Listings

Never settle for the first space you find. Comparing multiple properties gives you a better sense of market pricing, amenities, and lease structures. Create a spreadsheet or checklist to evaluate:

-

Price per square foot

-

Lease length and terms

-

Location benefits

-

Available amenities (parking, kitchen, conference rooms)

-

Hidden costs (maintenance fees, CAM charges)

Having multiple options also gives you stronger negotiating power when it's time to close a deal.

9. Negotiate Lease Terms

Commercial leases are complex, and terms are often negotiable. Don’t hesitate to ask for modifications that benefit your startup’s bottom line.

Key items to negotiate:

-

Base rent and annual increases

-

Rent-free periods (useful during the setup phase)

-

Who pays for utilities, maintenance, and repairs

-

Clauses for subleasing or early termination

-

Tenant improvement allowances for customization

Having a legal advisor or lease expert review your agreement can protect you from unfavorable conditions.

10. Consider Future Scalability

Your startup might be small now, but growth could come sooner than you think. Choose a space that allows for expansion if needed. Ask yourself:

-

Is there adjacent space you could lease later?

-

Can you easily reconfigure the interior layout?

-

Is the lease term short enough to allow relocation if necessary?

Planning for scalability ensures your space won’t become a constraint as your business evolves.

11. Evaluate the Surrounding Business Environment

The businesses around you can either drive traffic to your location or compete with you directly. Look for complementary services or industries nearby.

Examples:

-

A bakery near a coffee shop

-

A fitness studio near a health food market

-

A marketing firm near a coworking space

Your neighbors can even turn into strategic partners, making your location more valuable than it appears on paper.

12. Prioritize Accessibility and Parking

Convenience can make or break a business. If customers or clients struggle to find parking or access your building, they may choose a competitor.

Ensure the space offers:

-

Ample parking spots or nearby garages

-

Accessibility for people with disabilities

-

Proximity to public transit routes

-

Safe, well-lit walkways and entryways

Also, assess traffic conditions during peak hours to ensure the location stays accessible throughout the day.

13. Factor in Renovation and Setup Costs

Even if the rental rate is within your budget, modifying the space to suit your needs can be costly. Common expenses include:

-

Painting and flooring

-

Lighting upgrades

-

Installing partitions or fixtures

-

Internet and phone wiring

-

Furniture and equipment

Some landlords offer a tenant improvement allowance (TIA) to cover part of these costs—be sure to ask during negotiations.

14. Check for Hidden Costs

Don’t be blindsided by expenses not clearly outlined in the lease. Ask the landlord about:

-

Common area maintenance (CAM) charges

-

Property taxes

-

Trash and recycling fees

-

Elevator or security system maintenance

-

Snow removal or landscaping

Request a detailed breakdown of operating expenses so you can build a realistic monthly budget.

15. Time Your Move-In Strategically

The best time to move into a new space is when your startup is ready to maximize the opportunity. Don’t rush the move-in process. Instead:

-

Time it around product launches or marketing campaigns

-

Make sure utilities and permits are in place

-

Train staff and test systems before opening

-

Create a launch plan to generate buzz

Having everything in place before opening day ensures a smooth transition and sets you up for early success.

Conclusion

Choosing the right small business space for rent is a foundational decision that can affect every aspect of your startup—from customer acquisition to employee satisfaction and operational efficiency. By following the tips in this guide, you’ll be able to navigate the rental process with confidence and clarity.

The key is preparation: understand your needs, know your budget, explore multiple options, and never hesitate to negotiate. The right space doesn’t just accommodate your business—it supports it, enhances your brand, and gives you the flexibility to grow.

Your startup deserves more than just a place to operate—it deserves a space to thrive.

Categorii

Citeste mai mult

Well-reviewed parent super visa insurance: Your Comprehensive Guide Navigating the complexities of immigration and insurance can be daunting, but with the right information, it becomes manageable. If you're looking for Well-reviewed parent super visa insurance, you've come to the right place. This guide will walk you through everything you need to know, from understanding the basics to making...

Official website - https://reddyanna-ids.com/ Introduction to the Reddy Anna Book ID: Gujarat Samp Army and the Big Boys team The excitement is palpable as the Reddy Anna Book ID takes center stage in one of the most awaited matchups of the Legend 90 League 2025. This year, we witness an electrifying clash between two powerhouse teams: Gujarat Samp Army and Big...

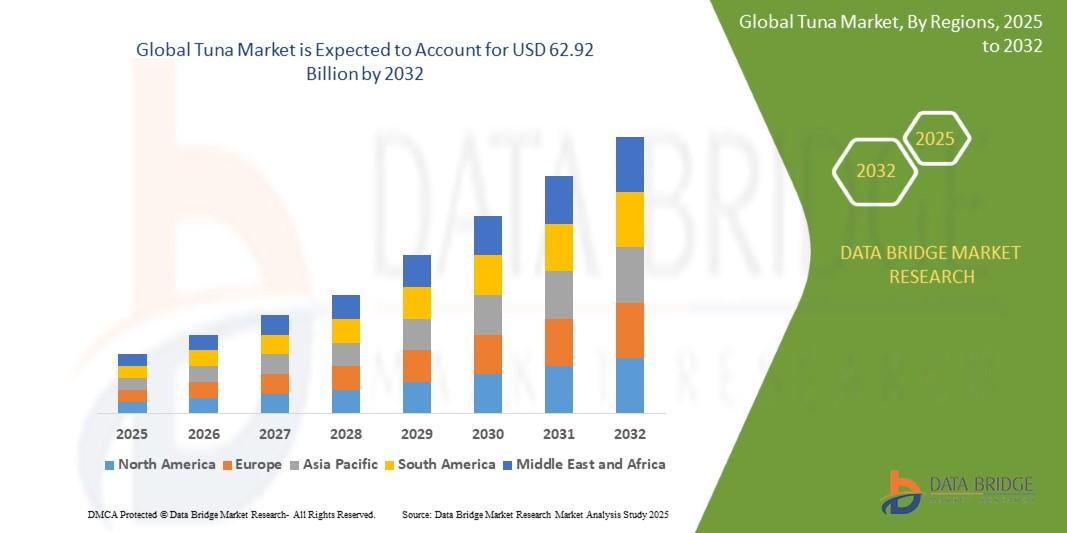

Tuna Market Size And Forecast by 2032 According to Data Bridge Market Research The global tuna market size was valued at USD 45.98 billion in 2024 and is projected to reach USD 62.92 billion by 2032, with a CAGR of 4.00% during the forecast period of 2025 to 2032. The extensive reach of Canned Tuna Market underscores its influence on a global scale. With an expanding customer base, Tuna...

Book Chennai to Chittoor cab online at best price. CabBazar provides car rental services for all cab types AC, Non AC, Hatchback, SUV, Sedan, Innova and Tempo Traveller. Both One way drop taxi and round trip cab available at lowest price. Price starts Rs. 9/Km.

A luxury dining table is more than just a piece of furniture; it is the centerpiece of your dining space, reflecting style, sophistication, and exquisite craftsmanship. Whether you love classic elegance, contemporary minimalism, or opulent statement pieces, a well-designed dining table sets the tone for unforgettable gatherings and fine dining experiences. Let’s explore the best luxury...